01

Decision lens

Three premiums in one price — pull them apart

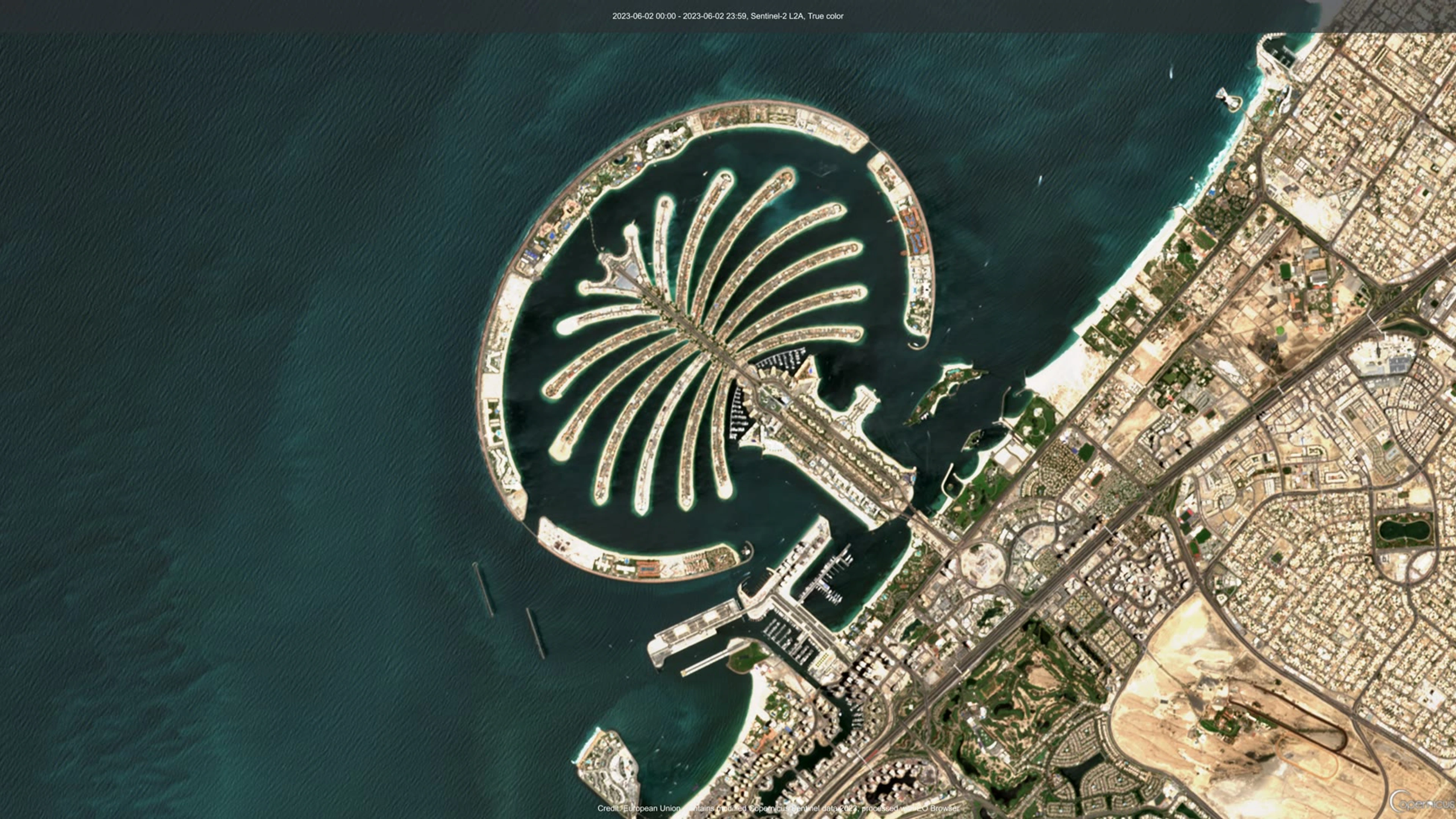

A branded residence on the Palm is paying for three things at once: the frontage (a Palm Jumeirah location), the brand (a hospitality operator's name and standard), and the service (the running quality of management and amenities). As a trusted advisor I read these separately because they age differently. The location premium is the most durable — it is the closed-island scarcity. The brand and service premiums are real but conditional: they hold while the operator performs and the building is run to standard, and they can erode if either slips. Underwriting the asset means asking which premium you are actually paying for and how secure each one is.